News & opinion

BCIS forecasts for the FM sector

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

24 September 2021

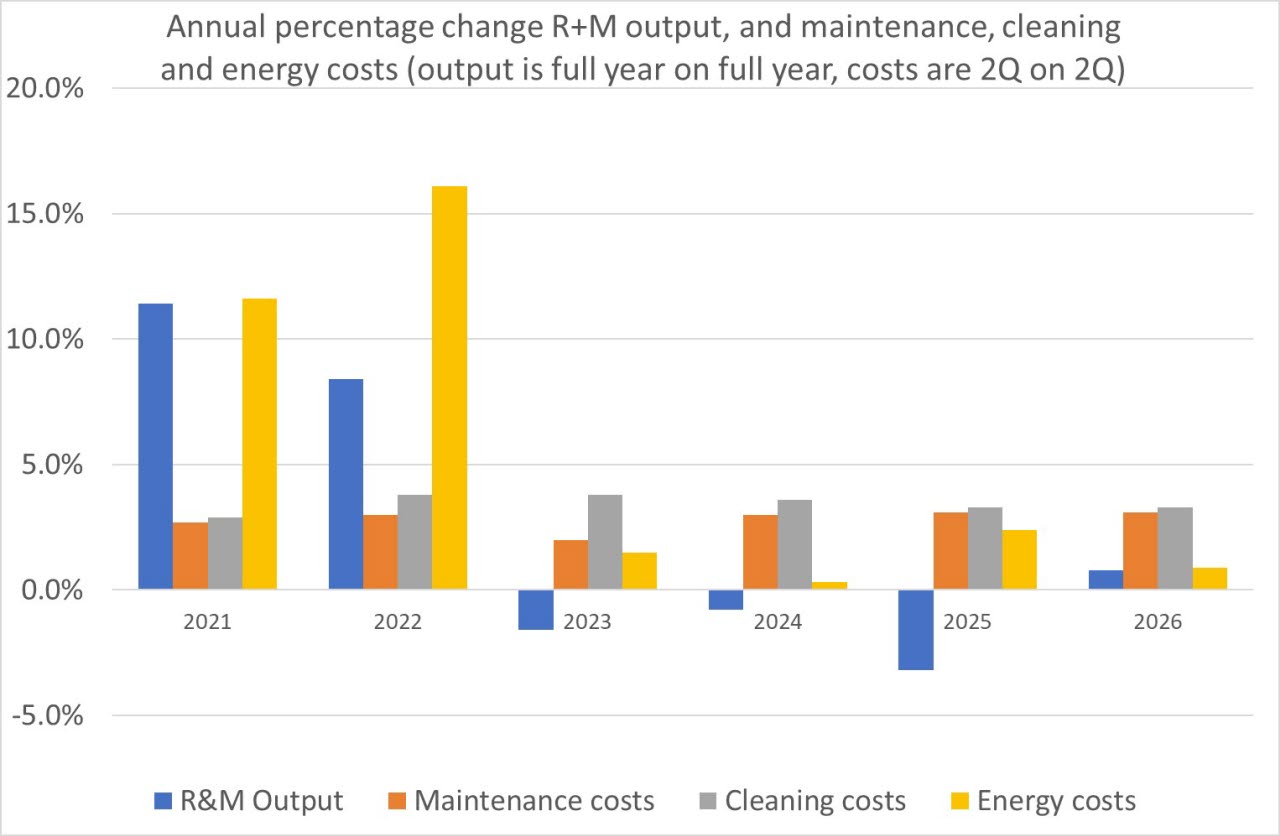

Interruptions, caused by the Covid-19 pandemic, have led to slumps and spikes in demand and supply. This has resulted in pressures on costs, particularly energy and some material costs. It is assumed that these effects will resolve themselves eventually, but they are expected to last well into next year.

The effect of Brexit on labour supply has been exacerbated by the Covid-19 restrictions on travel, and redeployment of furloughed staff which may put pressure on wages in the short term.

Over the forecast period (2Q2021 to 2Q2026):

- Maintenance costs will rise 15%: 3.0% increase in the year to 2Q2022, falling to 2.0% in the following year and then rising by around 3% in each of the following three years, mainly reflecting wage rises

- Cleaning costs will rise 19%: due to demand pressures as workplaces continue to open up, pressure on wages from increased demand generally and implementation of the National Living Wage (NLW). Costs are expected to rise 3.8% in the first two years of the forecast slowing to 3.3% thereafter.

- Energy costs are expected to rise by 22%, with large rises in oil and gas prices in in the year to 2Q2022 followed by modest increases over the rest of the period as the markets stabilise.

- R&M output is expected to grow just over 3% from 2021 to 2026. It will rise 8% between 2021 and 2022 as pent-up demand and alterations required by a new working environment push up demand. Output will decline slightly over the rest of the forecast period. The recladding of flats following the Grenfell fire will be included in the R&M output figures; an allowance for this has been included in the forecast.

The forecast is based on information available up to 28 August 2021.

No allowance has been made for the National Insurance contribution changes recently announced for April 2022.