India building sector outlook: What has contributed to the country’s standout growth?

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

12 June 2024

With India’s economy and the property sector in particular performing well despite global trends, the first of two articles asks: what key factors are behind its standout growth?

Authors

Donglai Luo, RICS economist

Vivek Rathi, head of research, Knight Frank India

Shilpa Shree, assistant vice president – research, Knight Frank India

India’s economy has performed well in recent years, in comparison with a relatively turbulent global picture. The country has seen consistent GDP growth and increasing foreign direct investment.

According to the RICS Global construction monitor (GCM), construction activities have remained robust, driven by strong domestic demand and supportive economic policies.

Indian economy proves resilient to pandemic and inflation

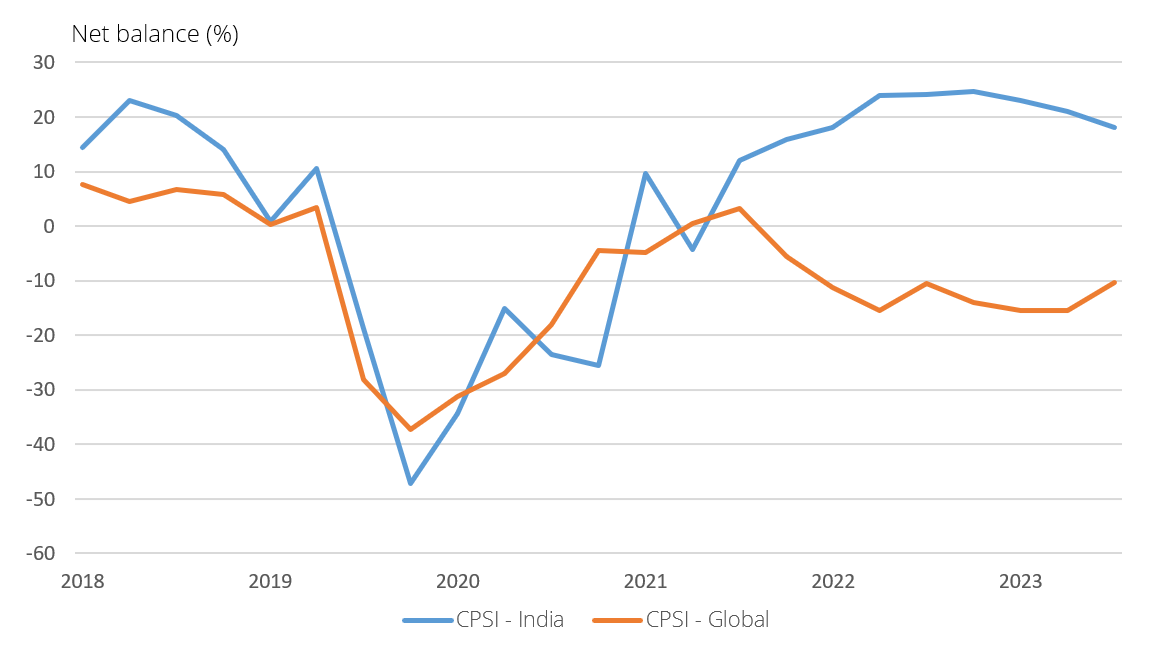

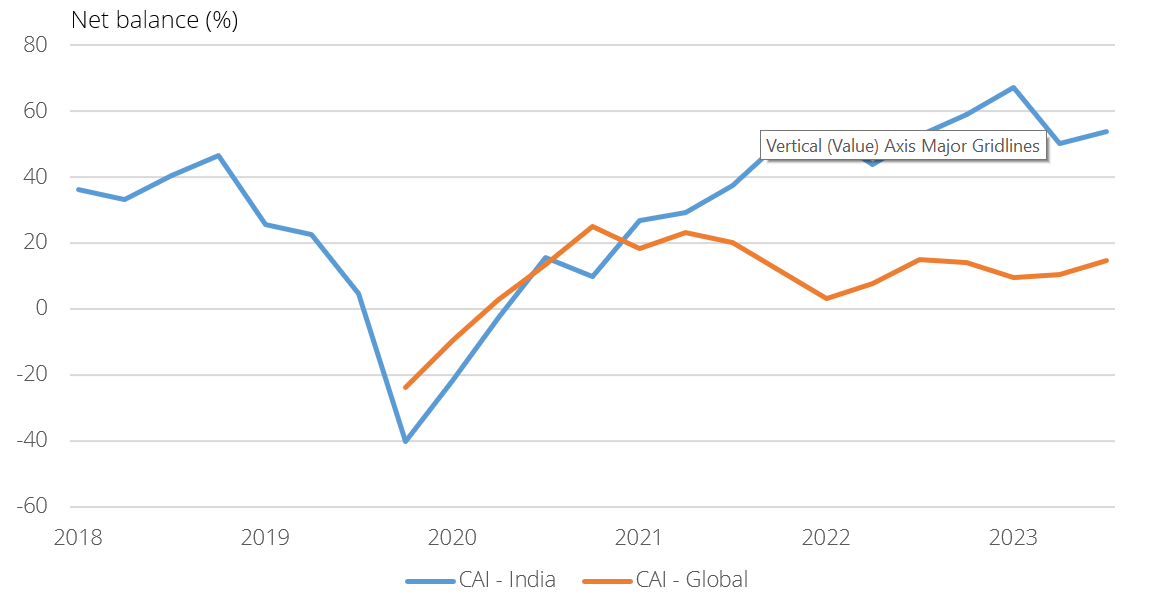

In contrast to the downturn in global real-estate markets over the past couple of years, India’s property sector has continued – and indeed continues – to perform relatively strongly (see Figure 1). This is evident in data on the construction industry (Figure 2) and transaction activity, and is clearly visible in the feedback provided for quarterly RICS sentiment surveys the Global commercial property monitor (GCPM) and the GCM.

Figure 1: Occupier sentiment as shown in the headline Commercial Property Sentiment Indices (CPSI). Source: RICS GCPM

Figure 2: Construction Activity Index (CAI). Source: RICS GCM

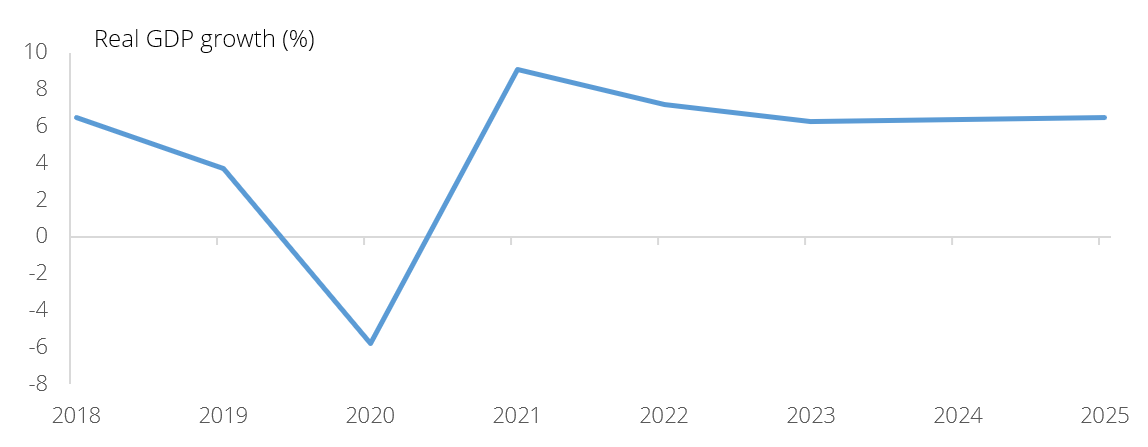

Like much of the rest of the world, the Indian economy was negatively affected by the COVID-19 pandemic, and at one point contracted by more than a fifth. However, according to World Bank estimates (Figure 3), it recovered within 12 months, with the real GDP growth rate rising to 9.1% by 2021. Since then, growth in India has consistently exceeded 6%, prompting institutions such as the IMF to revise projections for the country’s macroeconomic outlook in 2024 upwards to 6.8%.

Strong domestic demand underpins this optimistic forecast as the economy undergoes a critical phase of industrial transformation. Favourable tail-winds from international trade and investment also bolster the positive outlook.

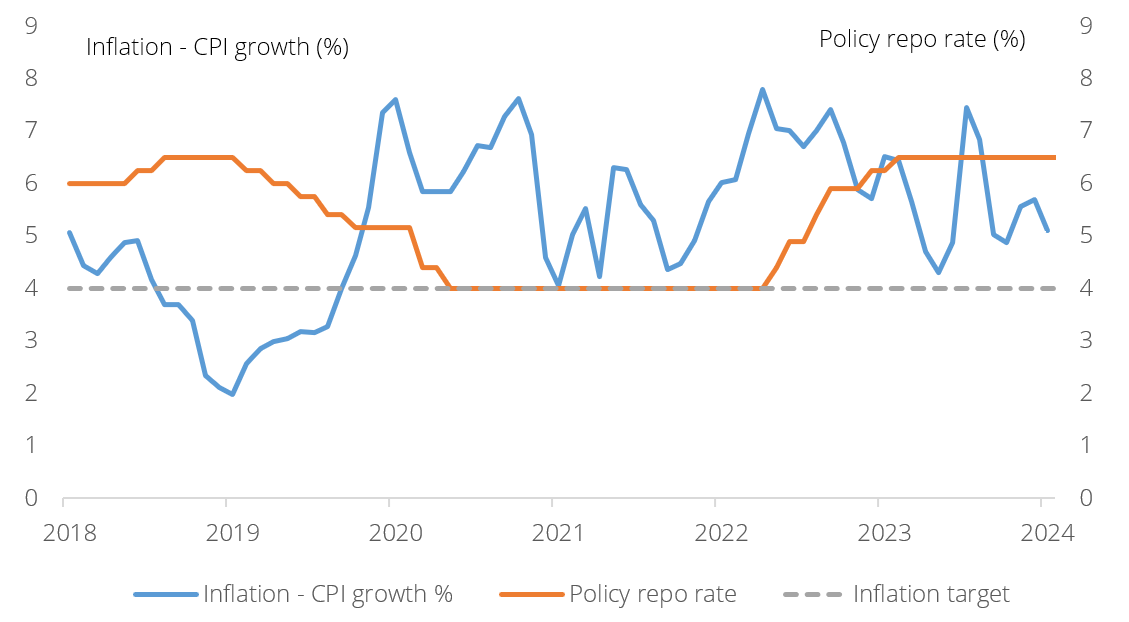

Interestingly, although interest rates have been sharply increased in India – as they have elsewhere around the world – Figure 2 highlights the relatively modest impact this has had on the country’s building sector, with its Construction Activity Index (CAI) starting to rise above the global figure at the same time as rates rose. Figure 4 shows the Reserve Bank of India (RBI) response to accelerating inflation, with the policy rate now back at 6.5%; incidentally, the same as it was in 2018.

The building sector’s ability to withstand this monetary tightening has been partly down to the resilience of national economic growth. This in turn has benefitted from a lower dependency on debt: domestic credit to the private sector stood at 90.1% of GDP in 2022, which contrasts with the related figures for other countries in the region as China’s dependency is at 219.5% of GDP, South Korea’s at 225.6% and Vietnam’s at 126.4%.

At its most recent meeting, the monetary policy committee of the RBI provided little indication that an early move in interest rates is likely. However, there is now a clear sense that the cycle has peaked and that the next move will be downward. That said, our suspicion is that RBI will not be in a rush to start easing the policy and that rates will stay close to current levels for much of the rest of the year.

Figure 3: Real GDP growth trend for India. Source: World Bank

Figure 4: Comparison of consumer price index (CPI) inflation and policy repurchase (repo) rate. Source: World Bank and RBI

Country remains attractive to foreign direct investment

Supply chain disruptions caused by COVID-19, as well as ongoing geopolitical developments, have led many businesses to begin to restructure their manufacturing networks in recent years. In this context, India emerged as a popular location for manufacturing, providing both macroeconomic and geopolitical stability as well as a workforce with the appropriate technical skills.

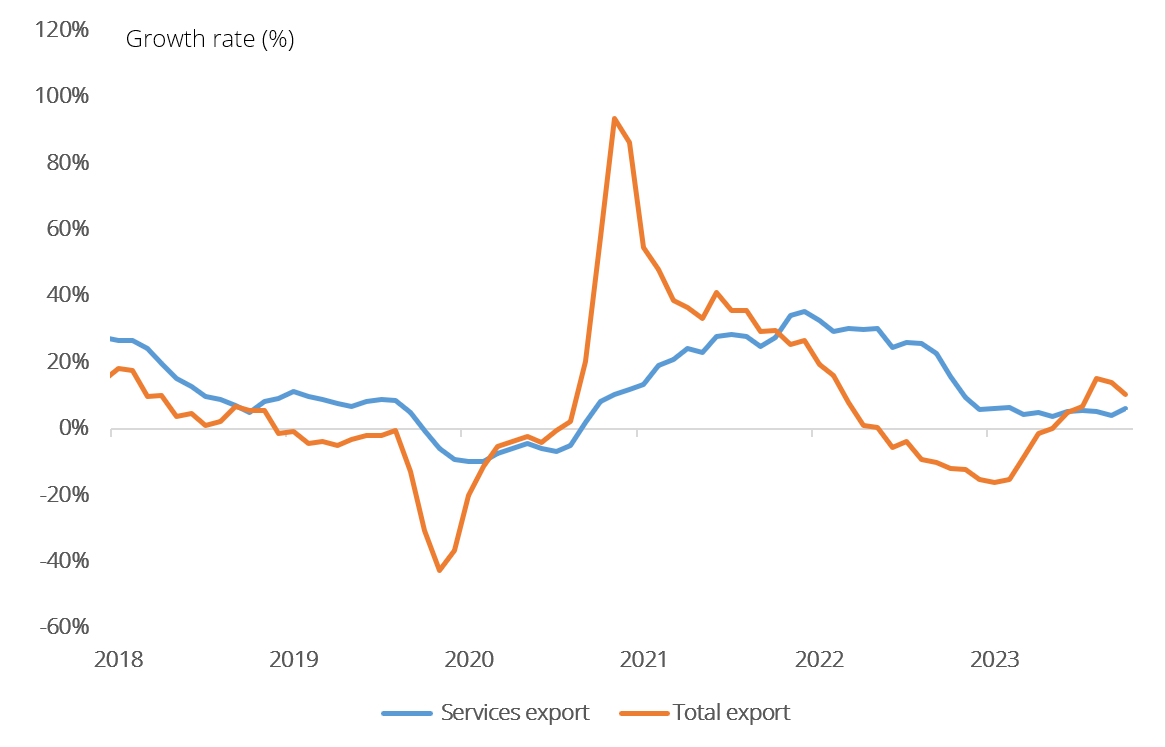

Despite recent decreases in export growth (see Figure 5), reflecting broader global trends, total exports have recovered and the export of services from India remains resilient. This may be in due in part to the so-called China plus one strategy, where large companies seeking to reduce risk in their supply chain have moved or diversified the location of their manufacturing away from China and into other countries, including India.

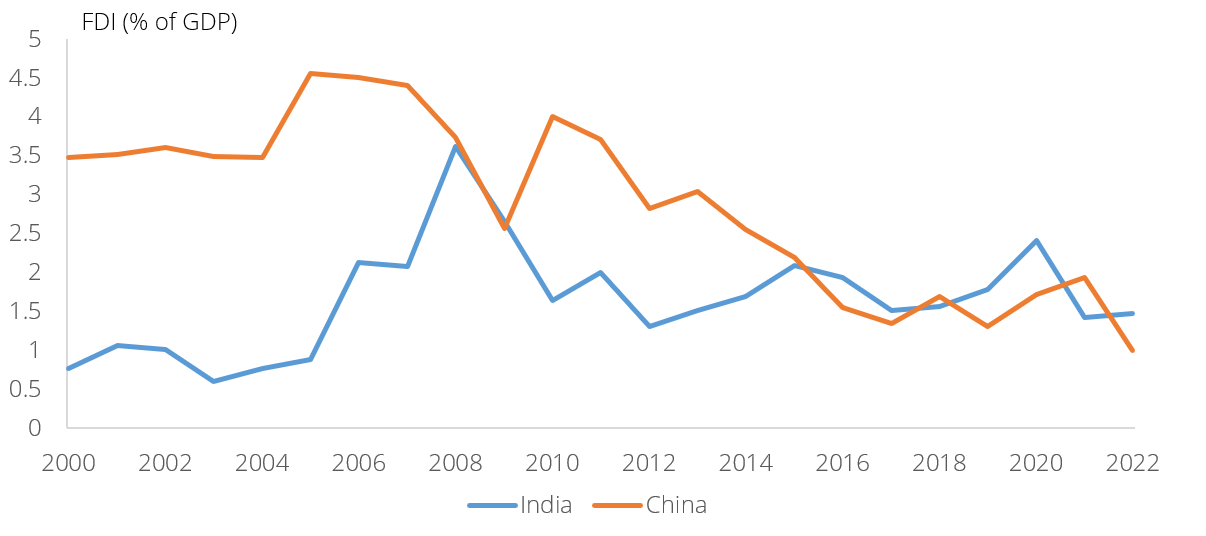

The more positive picture is also evident when it comes to looking at foreign direct investment (FDI) in India. As shown in Figure 6, the FDI contribution to GDP has remained strong in recent years, in marked contrast to similar data for China.

Looking ahead, the disparity between the two countries in terms of their appeal to FDI is expected to widen as India is likely to see such investment rise to more than 2% of GDP, according to Oxford Economics.

Figure 5: India’s export trend. Source: Indian Ministry of Commerce and Industry

Figure 6: FDI in India as a share of GDP. Source: World Bank

Service exports contribute to sustaining momentum

The data therefore suggests that India has remained relatively attractive as an investment destination in recent years.

Interestingly, it is the country’s traditionally strong service sector that has experienced the most significant boost due to this increased external demand, even as the China plus one strategy has benefited India’s manufacturing industry. On a broader scale FDI in India has remained robust, contributing to further GDP growth.

But while the Indian building sector has like the wider national economy outperformed other markets since the pandemic, can this momentum be sustained? The next article will look at this question in more detail.