Set for life

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

15 October 2019

The second edition of ICMS will have a major impact on life-cycle cost analysis, project reporting and facilities management

The World Bank and governments around the globe have incorporated both capital and life-cycle costs into their procurement decisions, so construction cost management and procurement is increasingly demanding a whole-life, value-for-money approach. However, there is currently no international standard for classifying and benchmarking costs across all types of project or throughout the life cycle of buildings or infrastructure – leading to discrepancies in the accounting process or in comparing and predicting project finances.

Life-cycle costs is vital to the financial management of construction projects and facilities management, representing a crucial consideration in whole-life cost decisions when income and non-construction costs, such as acquisition and financing, are included.

Life-cycle costs enable critical decisions to be made about the importance of capital and longer-term costs that could ultimately affect an asset's performance, longevity and how resilient it is. Other life-cycle costs could be part of facilities-related costs as well, such as environmental sustainability and occupancy costs such as subtenancy rent.

Recently published, the second edition of the International Construction Measurement Standards (ICMS 2) now includes other life-cycle costs such as asset renewals, operations and maintenance, and end-of-life costs. It has been developed through a process of extensive collaboration between industry representatives from 46 countries.

The second edition of ICMS brings life-cycle costs such as asset renewals, operations and maintenance into focus

Since the first edition, the principle of ICMS has been to ensure global consistency when classifying, defining, measuring, analysing and presenting the entire construction and other life-cycle costs, at a project, regional, state, national or international level.

Having a common cost classification structure linking buildings and infrastructure projects and the other facilities life-cycle costs will have a major impact on the way projects are designed, built and handed over for operation, then maintenance and renewal, through to end of life or during an investor's period of interest.

This should also have huge benefits for asset and facilities managers as it will enable stakeholders to compare costs on a like-for-like basis throughout the asset life-cycle. It will support clients formulating their sustainable estates and facilities strategy as well, by enabling control of the total ownership costs and ensuring robust analysis, benchmarking and understanding of where money is spent. This is especially important in economically challenging times.

ICMS2: Intended uses

• Construction and other life-cycle costs to be consistently and transparently benchmarked; that is, like-for-like comparative benchmarking at various stages of project life.

• The causes of differences in life-cycle costs between projects to be identified, informing options appraisals.

• Properly informed decisions on the design and location of construction projects to be made, ensuring the best value for money.

• Data to be used with confidence for construction project financing and investment, decision-making and related purposes, including forecasting annualised budgets for the other life-cycle costs in scope.

As property, construction and infrastructure continue to be increasingly global in extent and operation, there is a need for international consistency in fundamental life-cycle cost classifications. Historically, these processes have followed local and regional practice, making comparison across the world more difficult and leading to confusion, uncertainty and a lack of confidence among key stakeholders.

Globalisation of real estate only increases the need to make meaningful comparisons between countries, so stakeholders will benefit from a reporting system that provides internationally comparable life-cycle cost data. This will enable better financing decisions, optimum design and operation, a whole-life, value-for-money approach to procurement, and the bringing together of project and facilities financial management to give an overview of the whole-life cost of ownership.

As digitisation of construction proceeds at a rapid pace, ICMS's uniform international cost classification is required to enable new technologies to collect cost data, identify differences and interact seamlessly with design, environmental and operational data. The value of the standards is evident from the fact that the first edition was immediately adopted by the various technology companies in the development of cost, design and facilities management software.

Facilities managers and other stakeholders will greatly benefit from the second edition of ICMS

ICMS 2 will help facilities and asset managers in the following ways, including but not limited to:

• benchmarking historical life-cycle costs, such as renewals, operation and maintenance

• improved budgeting for future life-cycle costs and cost subgroups that are in scope during a project's post-construction phases

• sensitivity analysis of the impact that changes to particular project and facilities specifications have on life-cycle costing

• due diligence on business case decisions, from the perspectives of facilities management cost and affordability alike

• cost management of facilities management categories, namely operation and maintenance, asset renewals and other facilities management in scope

• demonstrating value for money over the entire asset life cycle, not just the lowest-capital project costs.

Informed clients need robust data and cost reporting for benchmarking purposes in order to assess the financial viability of their projects and whether it is affordable to operate and maintain, use and renew or dispose of them. Using ICMS, advisers on the capital construction project, life-cycle cost and facilities management can provide construction and cost information to their clients at various stages throughout each project's life, thereby improving cost certainty and enabling better-informed decisions.

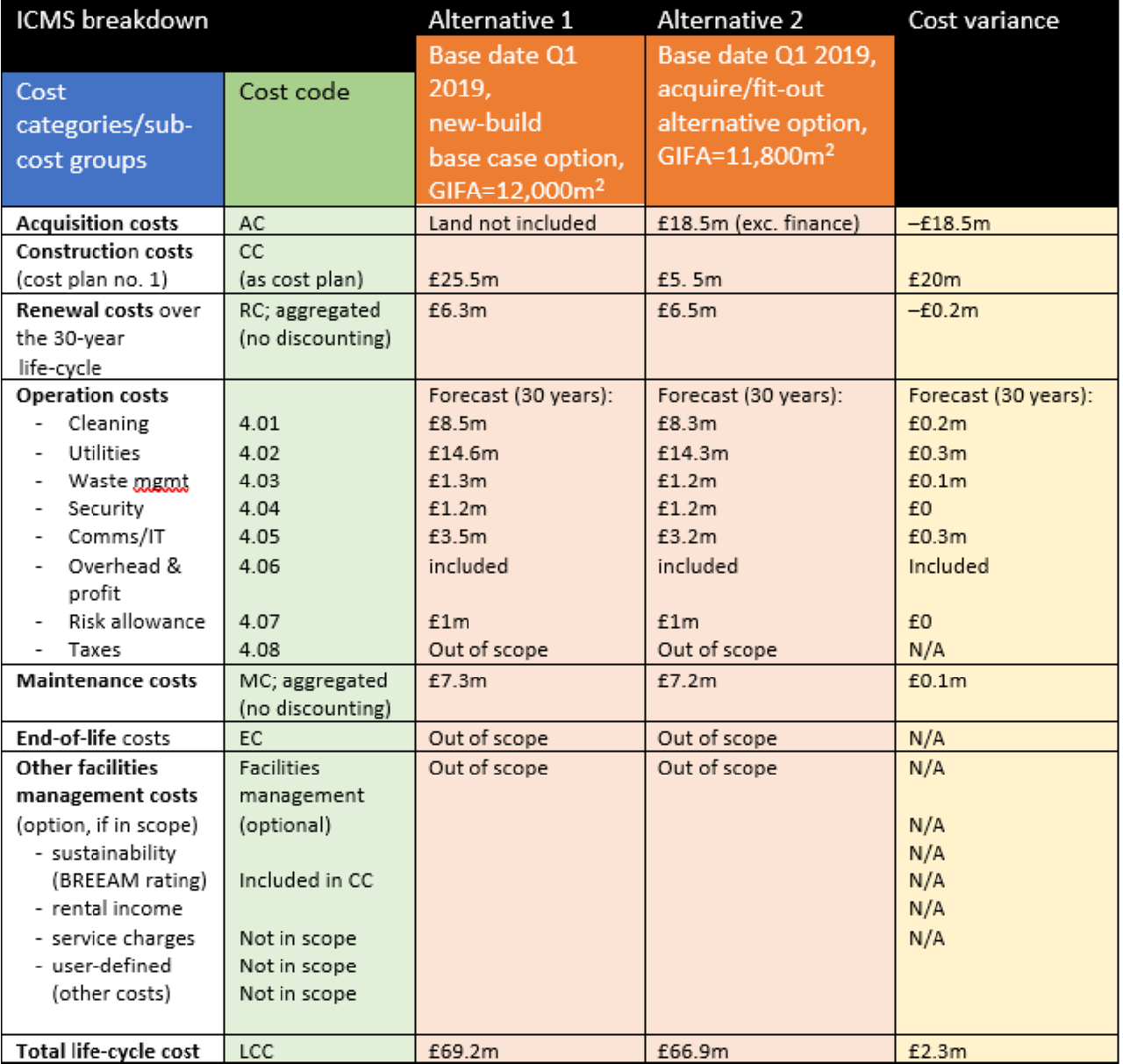

ICMS are designed to be used, where applicable, with building information models. Project values and attributes are designed to be used with drop-down lists to ease data input and subsequent analysis. It should be noted, however, that almost all building information models have the relevant data classification, such as Uniclass or Uniform 11, that is aligned to the New Rules of Measurement and also mapped to the relevant ICMS cost categories and subgroups. The worked example in Table 1 shows how ICMS 2 cost categories and sub-cost groups are typically used.

“Informed clients need robust data and cost reporting for benchmarking purposes in order to assess financial viability ”

As well as providing a high-level cost reporting tool, ICMS also have a cost classification function, such that individual cost groups or subgroups are, if applicable, set out, tabulated and totalled to arrive at the overall project and other life-cycle costs, plus any other facilities management costs agreed to be in scope.

Table 1 provides transparency on the capital costs and the other life-cycle or facilities management costs, in a format that enables easy comparison for analysis and benchmarking by cost categories and by sub-cost groups. This supports identification of the option that provides the best value for money, in terms of the total life-cycle cost, as well as setting the forecast budgets for running the facilities over the defined life-cycle period; in this case, 30 years.

Having a global standard for the presentation of construction and other life-cycle costings that can be embedded in building information models and other new technologies will transform cost information for projects. ICMS 2 will help to bridge the capital and revenue divide and enable the adoption of whole-life costing as the norm for future construction and related facilities management and procurement decisions.

Table 1: Worked cost breakdown of two project life-cycle options for an air-conditioned office

Andrew Green is RICS technical author of New Rules of Measurement 3, a member of the standards-setting committee for ICMS 2, vice-chair of the SFG20 technical standards committee, and director of Atkins: andy.green@atkinsglobal.com

This article originally appeared in the October-November 2019 Property Journal