Civil engineering tender prices are expected to rise in 2020

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

13 July 2020

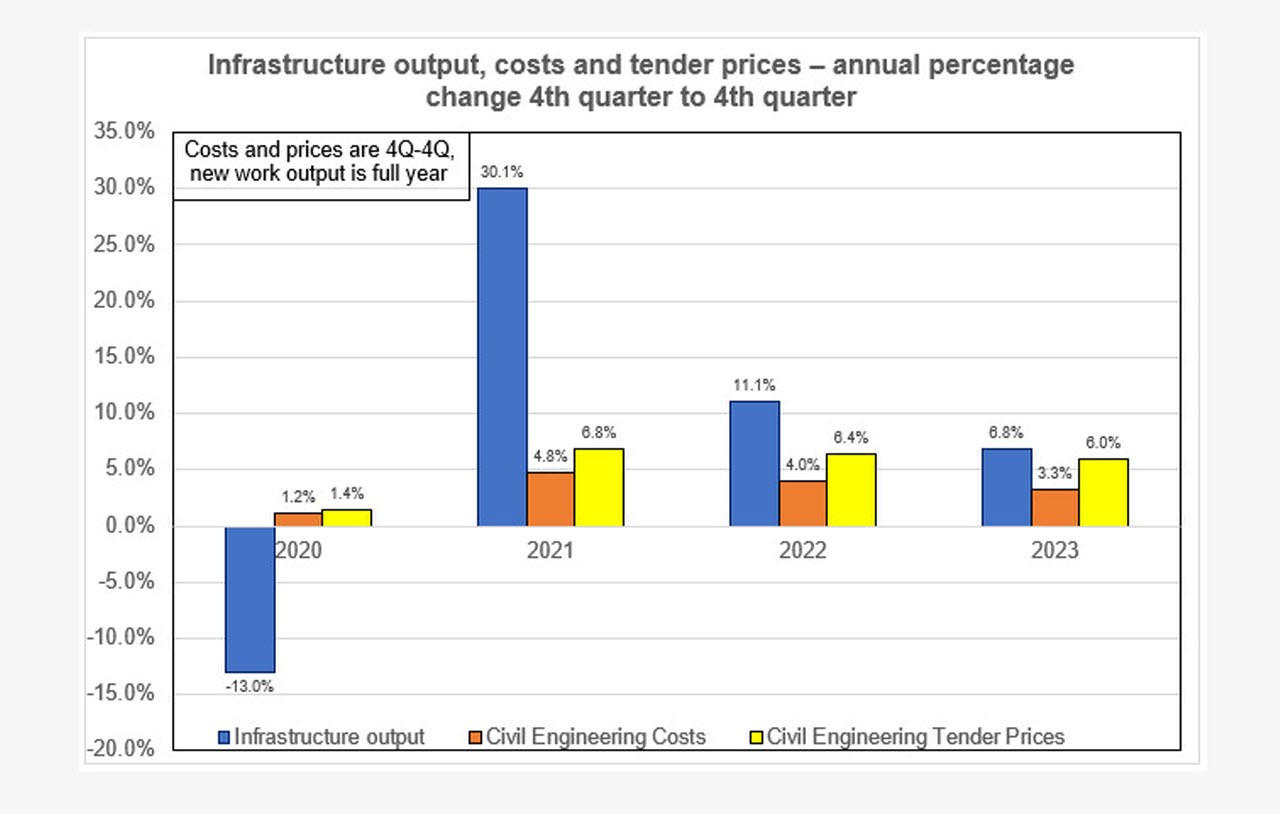

In 1st quarter 2020, the BCIS Civil Engineering Tender Price Index fell by 1.4% compared with the final quarter of 2019, but rose by 1.4% on an annual basis.

With a V-shaped recession and recovery in 2020, and with social distancing in accordance with the recent CLC publication Working Safely During COVID-19 in Construction and Other Outdoor Work (version 4), tender prices are expected to rise modestly over the first year of the forecast, by 1.4%.

With most work in civil engineering carried out in the open air, and not in confined spaces, the effect of social distancing is expected to be a lot less impactful than with building work. Also, local authorities have been given the power to increase daily working hours, and in some circumstances 24-hour working can be permitted to aid with social distancing requirements.

With the end of the Brexit transitional period set for the end of December 2020, and sharp growth in 2021 (largely a rebound from 2020), tender prices will be driven by strong input costs and the return to positive demand, rising by 6.8%. It is also assumed that social distancing will have eased. Over the remaining years of the forecast period, tender prices will be driven by strong output growth, and by input cost pressures, rising by around 6% per annum.

Over the forecast period (4th quarter 2019 to 4th quarter 2024):

- infrastructure sector construction output will rise by 48%

- costs will rise by 18%

- tender prices will rise by 30%

- UK Gross Domestic Product (GDP) will fall sharply in 2020 and grow sharply in 2021 as a result of the COVID-19 crisis. Over the following three years GDP will grow at a rate of 2 to 3% per annum

- annual general inflation rate will rise by 1% in 2020, and then by around 3% per annum over the remainder of the forecast period

- interest rates will rise gradually to 1.5% in 2023.

- Sterling exchange rates will remain depressed for the period of the Brexit negotiations

- the main risks to materials prices will be difficulty in obtaining materials during the COVID-19 crisis, oil prices, tariffs on imports and Sterling exchange rates

- nationally agreed wage awards are unlikely to increase over the next year, but will be affected by restrictions in the availability of European labour from 2021

- the COVID-19 virus crisis will dampen world demand and

- the forecast is based on information available up to 5 June 2020.

- The central scenario is based on the following assumptions.

- The COVID-19 crisis will lead to a sharp fall in new work output from March 2020 to August 2020 with a rebound after that.

- The UK left the EU on 31 January 2020 and a transitional period follows ending at the end of December 2020.

- During the transitional period, the UK continues to make payments to the EU (which will be deducted from the final 'divorce bill').

- It is assumed that following the end of the transitional period, any trade agreements with the EU are less favourable than before the EU Referendum.

- Sterling exchange rates are expected to remain depressed until around the midpoint of the forecast period, improving gradually thereafter.

- Free movement of labour continues to the end of the transitional period, with restrictions in movement after that.

- It is assumed that it remains desirable for EU workers to work in the UK and that demand for construction operatives in the EU remains unchanged.

- GDP growth remains between 2% and 3% during the second half of the forecast period.

BCIS has produced two other forecasts based on different scenarios, these are published in the full Civil Engineering Market Report available as part of the BCIS Civil Engineering Trends and Forecasts online service.