On 12 April 2025, 08:00 BST, we will be disabling logins for specific member-facing platforms to improve internal processes. We expect this to finish 12 April 2025 at 17:00 BST.

What next for the UK after Brexit?

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

12 November 2018

The UK is due to leave the EU on 29 March 2019, and we still have no clear idea what impact leaving the union will have on some of the most crucial aspects of our lives.

We rounded up a range of authoritative voices from across the residential, construction and rural sectors to find out.

David O’Leary

Policy director, Home Builders Federation

We’ve been working with our members for two years to evaluate the potential impact of Brexit, and three main areas of interest have emerged. The first is regulation and red tape: when we leave the EU, tendering processes could potentially be streamlined, and some environmental regulations could be eased somewhat. Those will be issues for us to try to influence in the future.

The second area is around materials and tariffs. In the worst-case scenario, if we were to exit the EU on World Trade Organisation rules, the cost of building an average home would increase by 2-5%, so that is not a huge game changer.

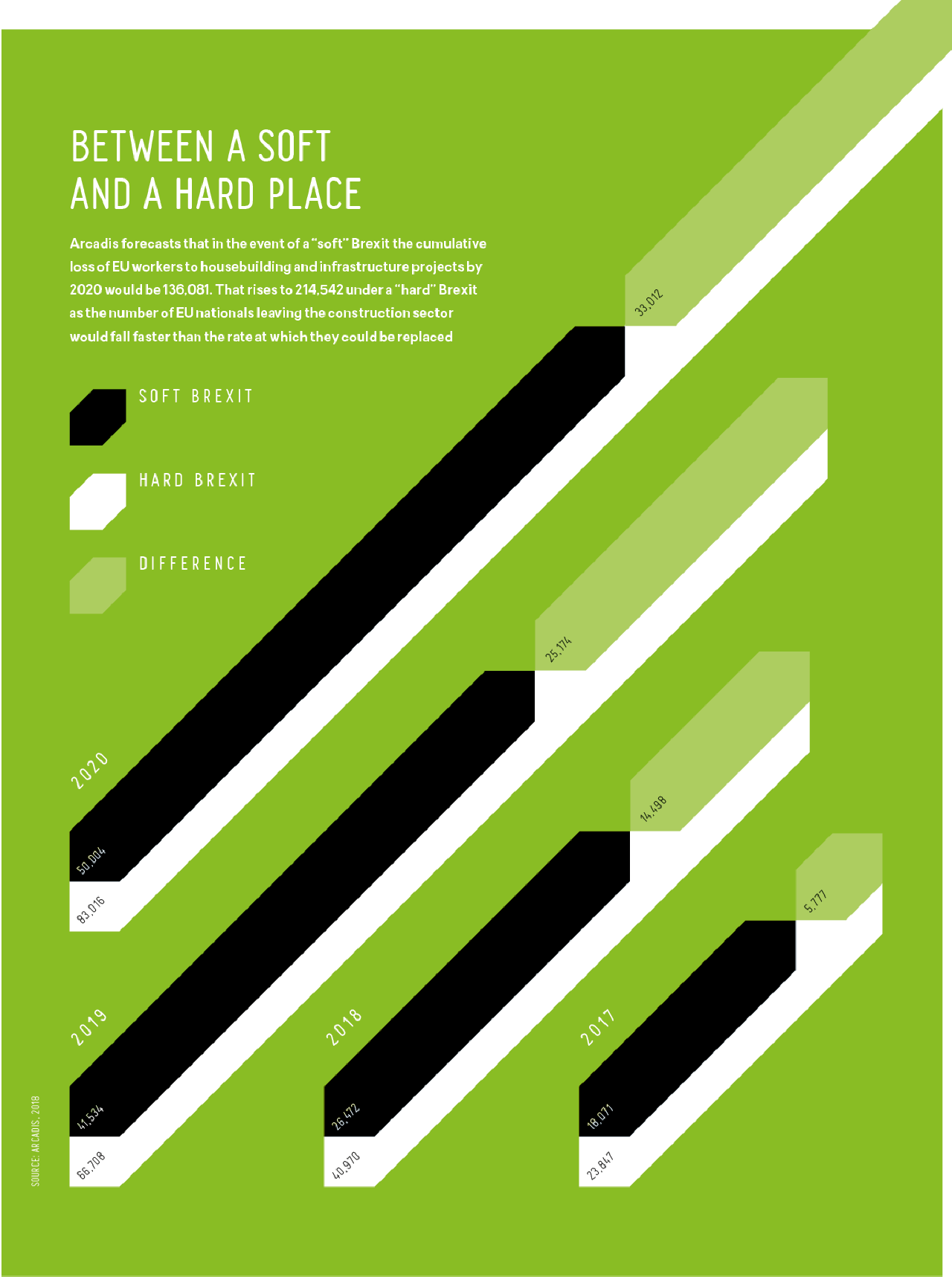

By far the biggest issue is labour and skills. The industry is facing quite a big skills shortage as it is. Late last year we did a census of the workforce covering about 1,100 housing sites and 38,000 people across the country. Around 20% of the workforce are non-UK workers, 18% from the EU, with Romanian workers by far the biggest group. There were huge regional variations, with sites in London having close to 60% overseas workers. The EU workforce also tends to be younger than the domestic one. We already have an ageing workforce, but without the EU workers that would be even worse.

Many people think of EU construction workers as transient, but we found many people had laid down roots in the UK. Provided their status is resolved adequately that gives us some cause for comfort. It is the additional workforce that enables us to expand output quickly that is more likely to be affected. The industry is doing a lot to train and recruit a domestic workforce, but it is difficult, and we need to work hard to change the image of housebuilding as a career. The Brexit transition period will help to buy us some time on that front.

Liam Bailey MRICS

Global head of research, Knight Frank

The feedback from our agents is that Brexit is an issue that is weighing on the minds of purchasers and even vendors. Any economic uncertainty tends to lead to a slowdown in the housing market because people are more reluctant than normal to make big decisions.

My feeling is that after March 2019, regardless of whether we have a deal in place, people will begin to take action again. In the past when we have seen uncertainty delaying activity, an event generally comes along that unlocks that activity.

The evidence so far is that the economy has tended to ride out the process of Brexit fairly well. The prime market in the capital has experienced a slowdown with prices falling 10-15% in central London, but Brexit is only part of that story. The main issue at the upper end of the market has been the increase in stamp duty.

If there is a no-deal Brexit and sterling falls significantly, then we could see an influx of overseas investors, and if the economy slows then interest rates might stay lower for longer, which would be a boost to the housing market, although that would be offset by weaker growth.

Will Waller

Head of futures, Arcadis

The UK will continue to be an attractive place to invest in both the short and long term, regardless of the type of deal it strikes with the EU.

If you take a world view, Brexit is actually a relatively manageable political risk, which probably puts the UK in a similar political and trading position to many other successful countries. It’s true that we might expect further devaluation of sterling, but for an investor outside the UK, this makes the country a more attractive place to put their money because they can get more for it.

However, when you start to look at how infrastructure schemes will actually be financed, the picture becomes murkier. Across all the most likely Brexit scenarios, there is an implication that the UK will cease from being a member of the European Investment Bank. While that doesn’t mean the UK necessarily loses access to EIB finance, it does imply a change in terms and probably higher borrowing costs. This is significant because the EIB has lent about £35bn to UK infrastructure projects since 2011. EIB money has been pivotal in leveraging other private finance as it allows investors to get more comfortable with the risks attached to schemes, so clearly this is a concern.

What plays out will depend on the final deal but, either way, industry can still work together to boost “investability” by collaborating to reduce and share risk and involving investors early on. This could all help to maintain the attractiveness of UK infrastructure as an investment opportunity.

Anthony Breach

Analyst, Centre for Cities

Under a soft Brexit, our research shows gross value added per head falling by around 1.2% in the average local authority. Under a harder Brexit, that goes up to 2.3%.

In the long run, cities such as London and Cambridge will be able to adapt to the changing conditions that Brexit produces because they have diversified economies and a skilled workforce.

Cities with less skilled populations will be impacted more severely. That will mean a reinforcement of existing patterns in economic performance, so the patterns that we see across the UK housing market will also stay the same or be reinforced.

Matthew Watson MRICS

Director – rural, Savills, York

Brexit doesn’t necessarily spell bad news for farmers. If someone has a successful business now, there’s no reason why it won’t continue to be a success in future. The key will be for people to understand what they want their business to do so they can respond to whatever changes are coming.

Post-Brexit, agriculture doesn’t necessarily have to involve four legs or be grown in a field; land management can be just as important. As part of that there’s no harm in focusing on the environment as part of the business, as farmers with marginal land or small enterprises might see more benefit from focusing on natural capital rather than food production.

There’s often a temptation in agriculture to watch from afar and see what happens, but Brexit is one scenario where we have to be on the front foot and not the back.

James Sammon FRICS

Director, Sammon Chartered Surveyors, Northern Ireland

With the construction industry in Northern Ireland already on its knees, there are fears that a loss of freedom of movement as a result of Brexit will make matters worse – not to mention the effect it will have on our wider economy.

High numbers of construction workers already have no option but to travel to Britain and Dublin every week for work. Just think of the impact these absences have on the families and communities of those who have to leave. A direct consequence of this exodus of workers is a loss of local skills training – another area that will be hit particularly hard by Brexit. And with less opportunity to build a local skills base, the industry is likely to struggle further.

Meanwhile, there are fears that changes to exchange rates, tariffs and border controls will reduce competitiveness and the industry’s ability to trade. This is stoking concerns for those directly involved in construction, as well as those indirectly involved such as businesses or potential investors, who may commission construction works. Northern Ireland depends on a considerable annual net subvention from Britain and is at risk if the national economy weakens as a result of Brexit.

I see no evidence that Britain will build better trade relationships than those which already exist within the EU. I see much more evidence of unproductive expenditure around the Brexit effort and around prospective border controls, which has the potential to take on a life of its own.

Neal Hudson

Director, Residential Analysts

A no-deal Brexit would be economically disastrous because there has clearly been very little planning for how we would cope in that scenario. It is likely that there will be an economic shock, and we may well see a run on sterling, together with an increase in inflation and rising interest rates. If that is the case then instead of cutting rates to provide a boost in a downturn, we may see the Bank of England increasing them to protect the economy.

Currently, the Bank of England expects to increase rates slowly to allow people to adjust, but if they were to rise sharply by 4-5% that would cause a lot of pain for a lot of people – particularly in London and the south-east, the markets that have recorded the strongest growth. Prices could fall by as much as 25-30%, like they did in the early 1990s recession.

Meanwhile, job losses as a result of an economic shock could also have a catastrophic effect on the housing market in other parts of the UK. First-time buyers might welcome a house price crash, but if the underlying economy is weak, they may not be able to find a job to get a mortgage, or a bank willing to lend.

Edward Dixon MRICS

Partner and head of rural, Knight Frank, Bristol

The general feeling in the industry towards Brexit is positive. Farmers are looking forward to having more control in terms of how the UK’s countryside and agricultural industry is managed, rather than being dictated to by Brussels.

While there is positivity though, there are obvious challenges. Subsidy reform will be the biggest change, as we’re coming out of the Common Agricultural Policy and leaving funding arrangements that have been in place for decades. Our farming businesses have been set up around the CAP and, since the Second World War, Europe has dictated in many respects what and how much is grown.

Trade will also be a major issue, particularly in the event of no deal being reached. Agriculture is such a small part of the UK’s GDP that there’s a real question of where it will stand in trade negotiations. In the short term, the consequences of that could be difficult: the UK’s infrastructure is set up for more export and less processing. But, hopefully, with more people thinking about home-grown produce and buying British, there will be more processors who will step up and take on that role in the long term.

As part of the changes, in order to trade farmers will need to get closer to markets to understand for whom they are producing. There will be new markets for them to take advantage of – both in terms of what they produce and who they trade with – but they will have to engage with them.

Whatever is agreed, though, the short term won’t be easy. Brexit will change the structure of the industry, and there will be people who will lose out. Those who have always collected their subsidy without really thinking about where their business is going, or where their future lies, will be obvious casualties.

Julian Jessop

Chief economist and Head of the Brexit Unit, Institute of Economic Affairs

A lot will depend on the form that Brexit takes. In the short term there is no doubt it will be negative for the British economy. I think that leaving is the right thing to do, but even I would admit that the level of GDP is perhaps 1% lower now than it would have been if we had voted to remain in the EU.

My hope is that we will negotiate a Brexit in which we leave the single market and customs union but continue to have a close relationship with the EU and a comprehensive free trade agreement. In that scenario I don’t think there will be a big impact on the wider economy or the housing market.

A no-deal Brexit where we are trading on WTO rules will also have little overall impact on growth in the long run, but in the short term it might lead to fresh uncertainty. For ordinary people a house is the biggest-ticket item they are ever going to buy, so if the process of leaving is messy then the housing market will suffer as people put plans on hold until things settle down.