Global Construction: The state of the industry in three graphs

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

29 September 2021

The quarterly RICS Global Construction Monitor charts sentiment across the industry. Ahead of the release of the Q3 2021 survey, we review results in the last quarter. Is the build back better movement making any difference?

The results of the Q2 2021 RICS Global Construction Monitor suggest that some structural challenges in the sector could outlast the worst of the COVID-19 crisis.

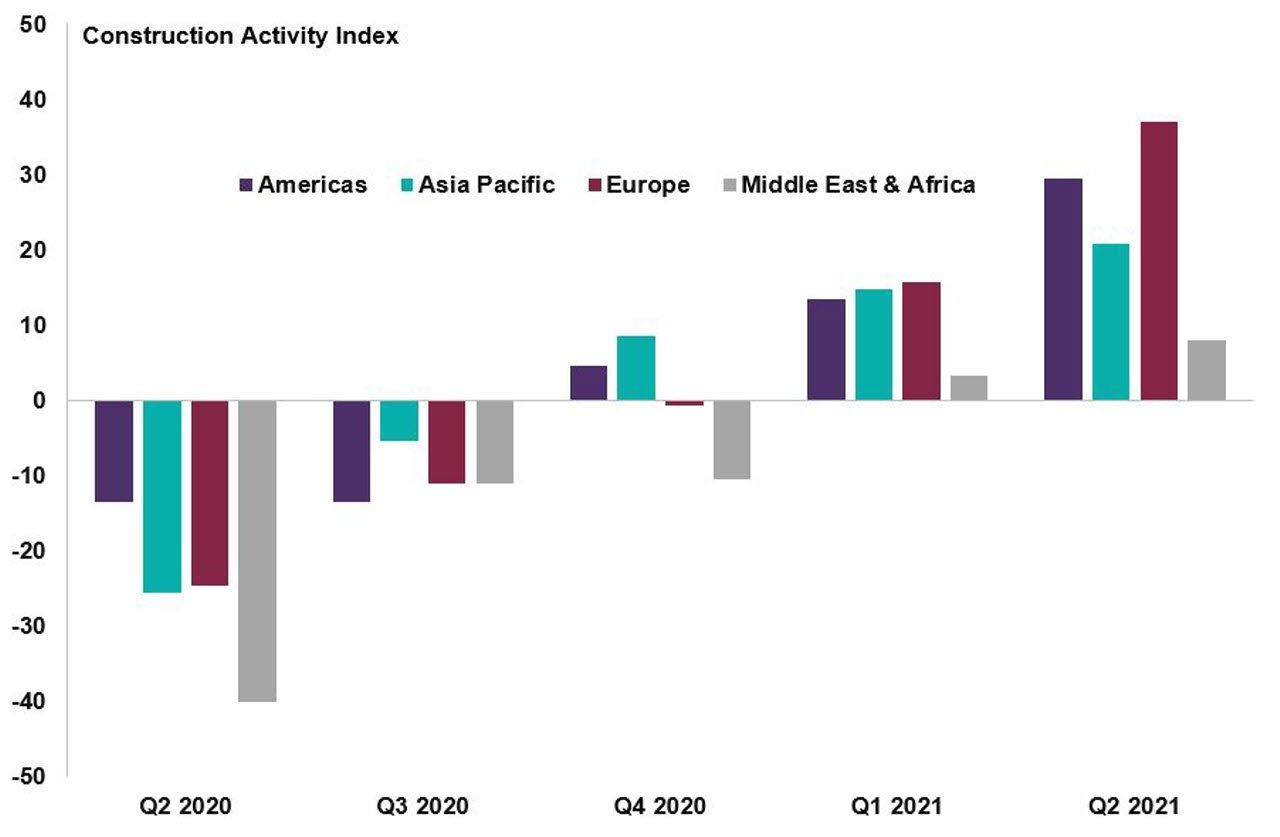

Construction Activity Index

First, the good news. Q2 2021 was the second consecutive quarter in which survey respondents reported an uptick in activity across all surveyed global regions. And nowhere is the picture rosier than in Europe. Back in Q4 2020, the continent lagged Asia Pacific and the Americas, where the green shoots of signs of recovery first took hold. Sentiment has changed markedly since the turn of the year.

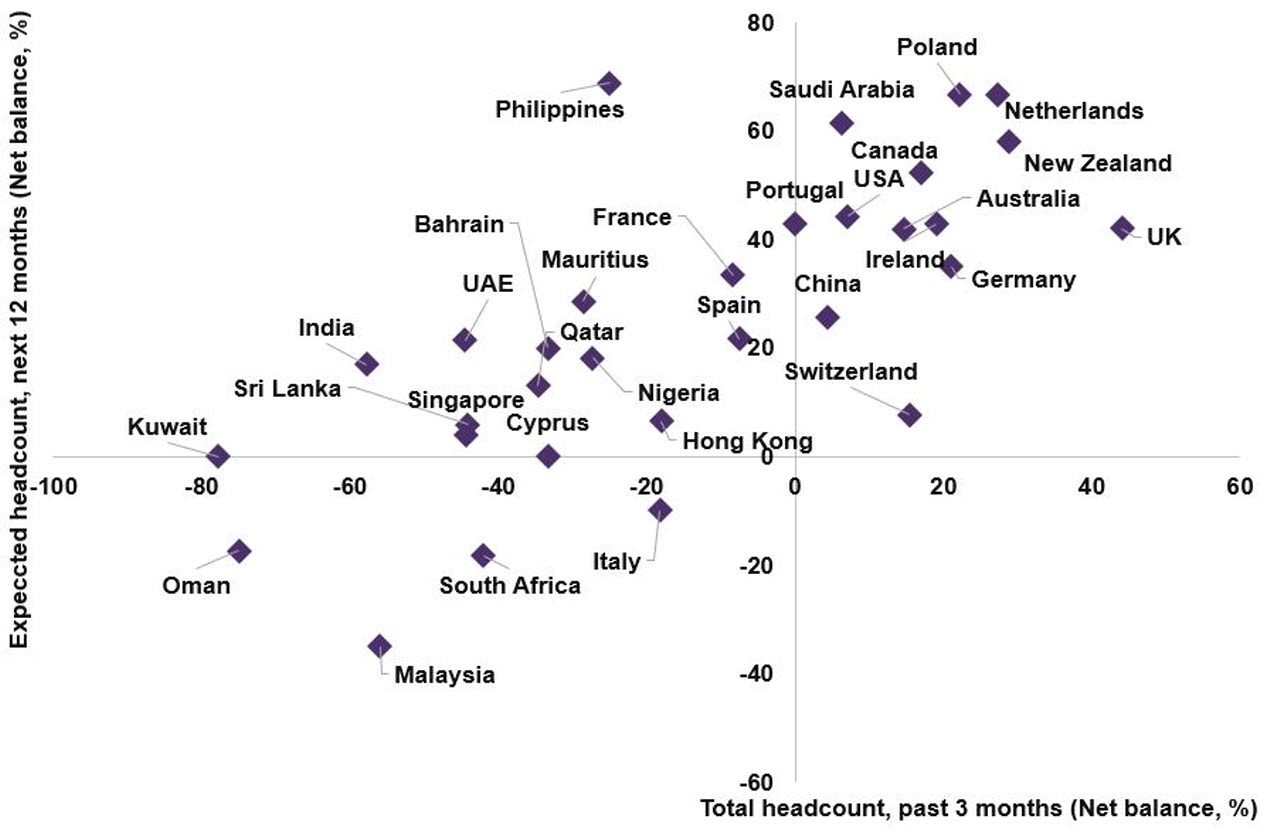

Current and expected headcounts

Current and expected headcounts

Estimates suggest that nearly 9% of the world’s total labour force works in the construction industry ecosystem. The good news for the global economy is that, in most countries across the world, headcounts are expected to grow over the next 12 months. However, in the three months April – June 2021, most respondents were still waiting for that boost in labour power to manifest. In four markets, Italy and South Africa among them, already depressed headcounts are expected to fall further over the coming year. Those in search of work in the sector could do worse than look to Poland and the Netherlands, where the expectation is for abounding employment opportunities.

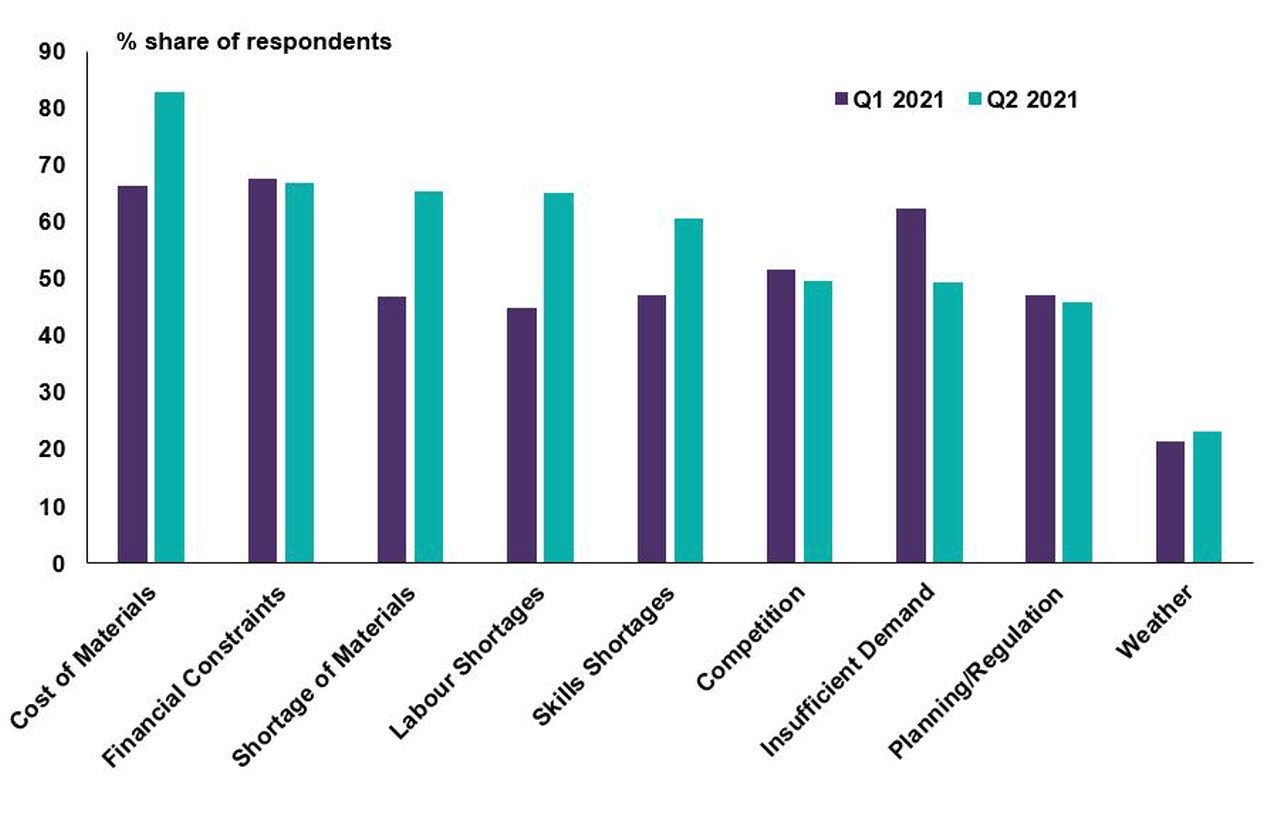

Factors holding back activity

Factors holding back activity

Globally, 83% of respondents highlighted the cost of materials as having an inhibiting effect on activity, while 65% also flagged limited materials availability as a concern. There can be little doubt, then, that the disruption to global supply chains caused by the pandemic is showing few signs of easing. Labour and skills shortages were also cited by a growing number of respondents, suggesting that restrictions on the movement of people, as well as goods, are hurting productivity in the sector. Cause for encouragement comes in the form of the falling number of participants reporting stagnating market demand for construction services.