Facilities Management: The state of the industry in five graphs

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

17 February 2021

The Facilities Management profession is likely to find itself increasingly under a microscope as governments move cautiously towards the easing of lockdowns, and employers reassess existing workplace arrangements. As early as May, with the crisis unfolding, then RICS President Elect Kathleen Fontana was moved to praise the sector for its “astoundingly responsive” actions. With much of the western world entering a second year of COVID-19 restrictions, the industry view seems more relevant than ever. Here, we chart how opinions moved over the last year on five questions of key importance.

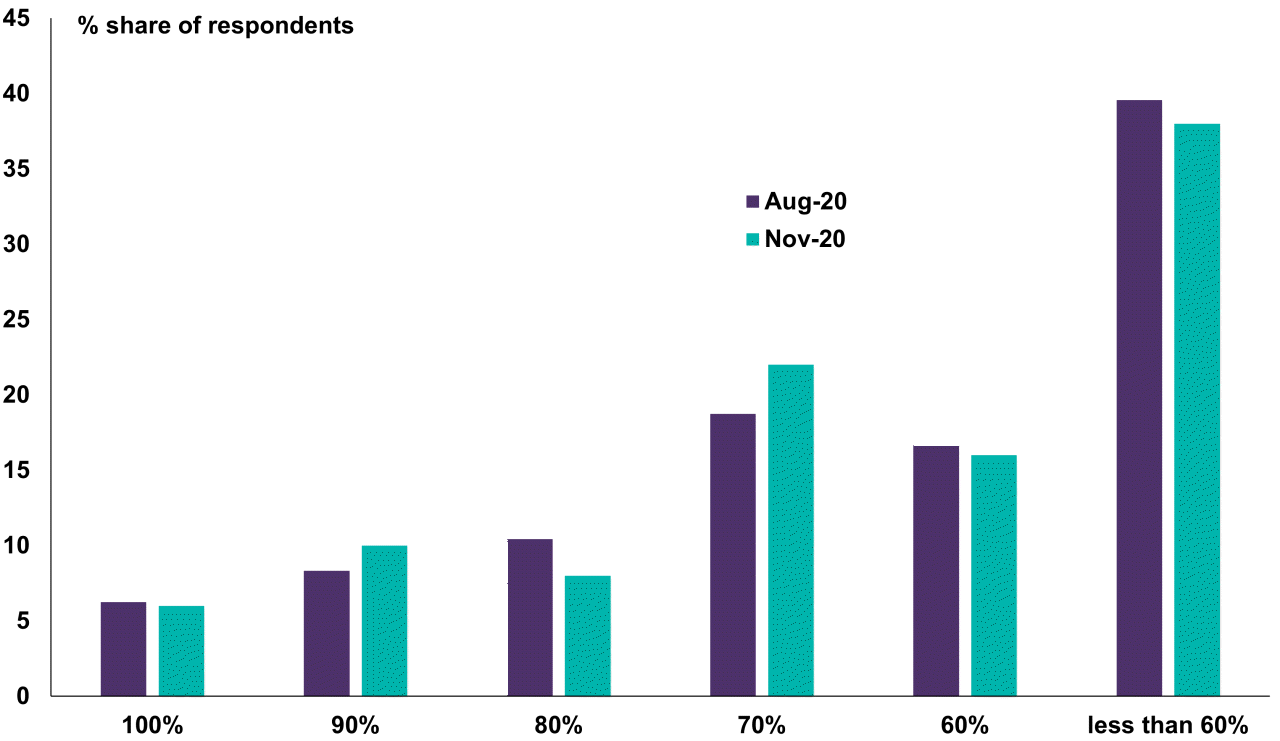

What proportion of the workforce do you expect to return to the workplace as normal once COVID-19 restrictions are lifted?

First introduced to the RICS Facilities Management survey in Q2 2020, responses remained remarkably consistent over the three quarters to year end. At each time of asking, a majority of respondents answered in the 60% or less range. Consecutive surveys did see growth, albeit modest, in the number of respondents expecting workplace capacities to reach 70%. Crucially, the number of respondents expecting the entire workforce to return to the workplace has never yet exceeded single-digit percentage points. The prospect of getting back to business as usual seems extremely remote.

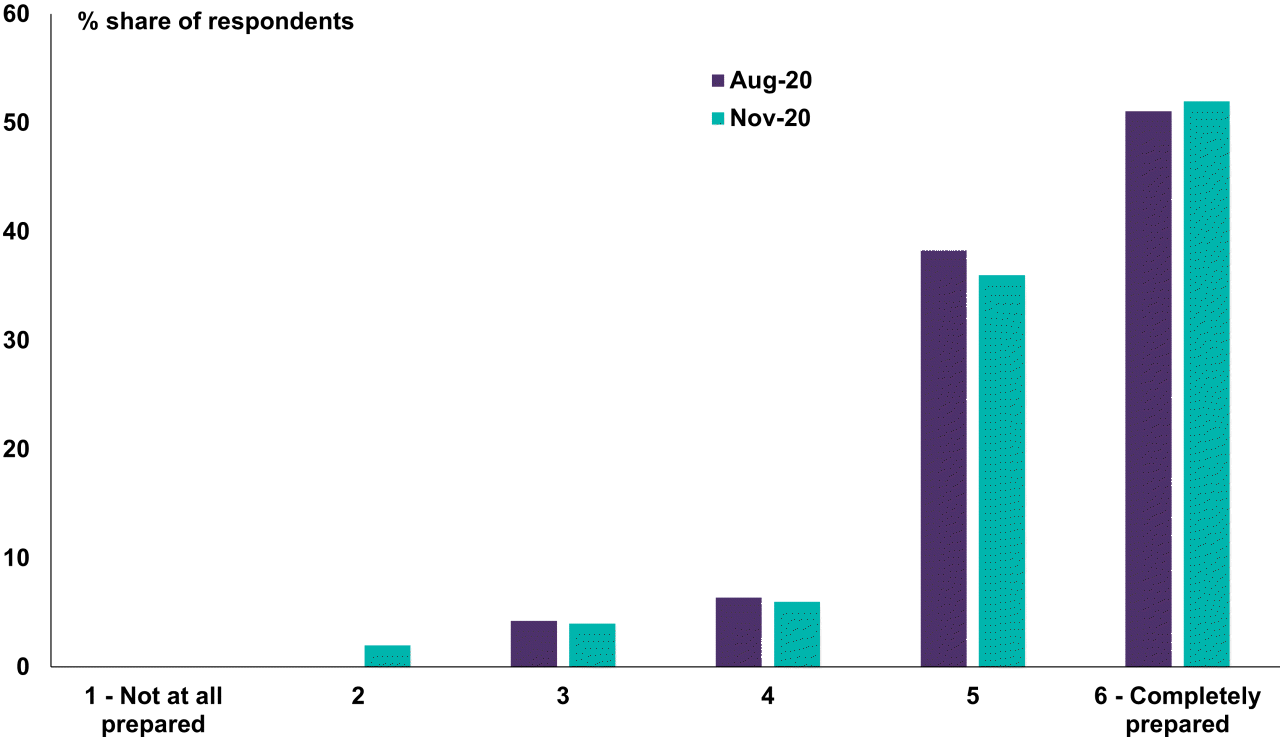

Are your buildings now fully setup to operate with physical distancing measures in place?

Encouragingly, the industry reports itself ready to welcome workforces back to socially distanced workplaces. 51% of respondents declared themselves completely prepared for the realities of physical distancing when the question was first asked in Q3. That number crept up slightly in Q4, with many more respondents telling us that they are almost completely prepared.

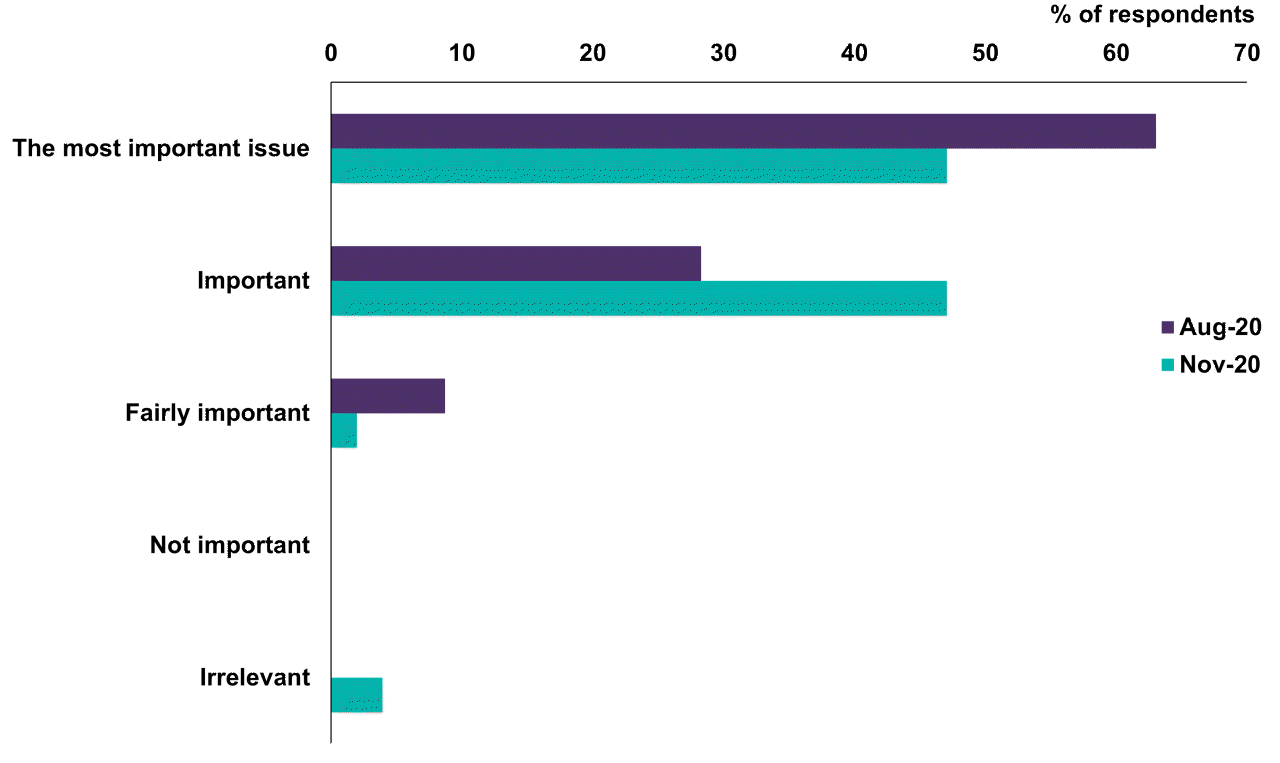

To what extent do end users consider sustainability in tendering processes?

In the first half of 2020, we were told that 80% of end users rated sustainability as either an important consideration or the most important consideration in tendering decisions. In Q3, the number jumped to 90%, boosted by a surge in respondents (>60%) saying their end users regarded sustainability as the most important factor. While the breakdown between important and most important evened off in Q4, the overall tally remained around 90%. COVID-19, it seems, is rightly regarded as an environmental, as well as a public health crisis.

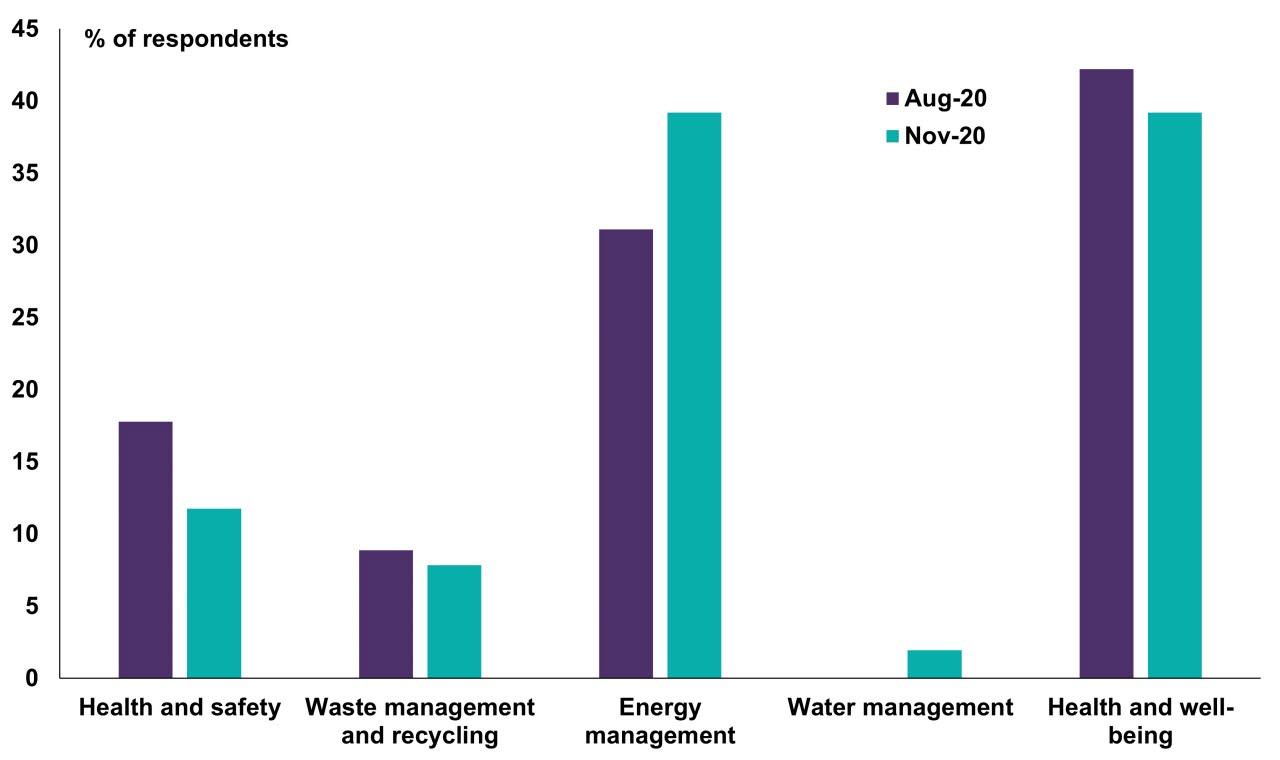

Which areas of sustainability have seen the strongest growth in investment over the past twelve months?

Over the course of the year, Energy Management and Health and Wellbeing have vied for the top position, to the exclusion of all other categories. Conversely, Water Management polled fifth out of five in each of the four quarters, with 0% of respondents reporting strong investment growth in Q2 and Q3. This apparent blind spot is one for the industry to monitor closely in 2021.

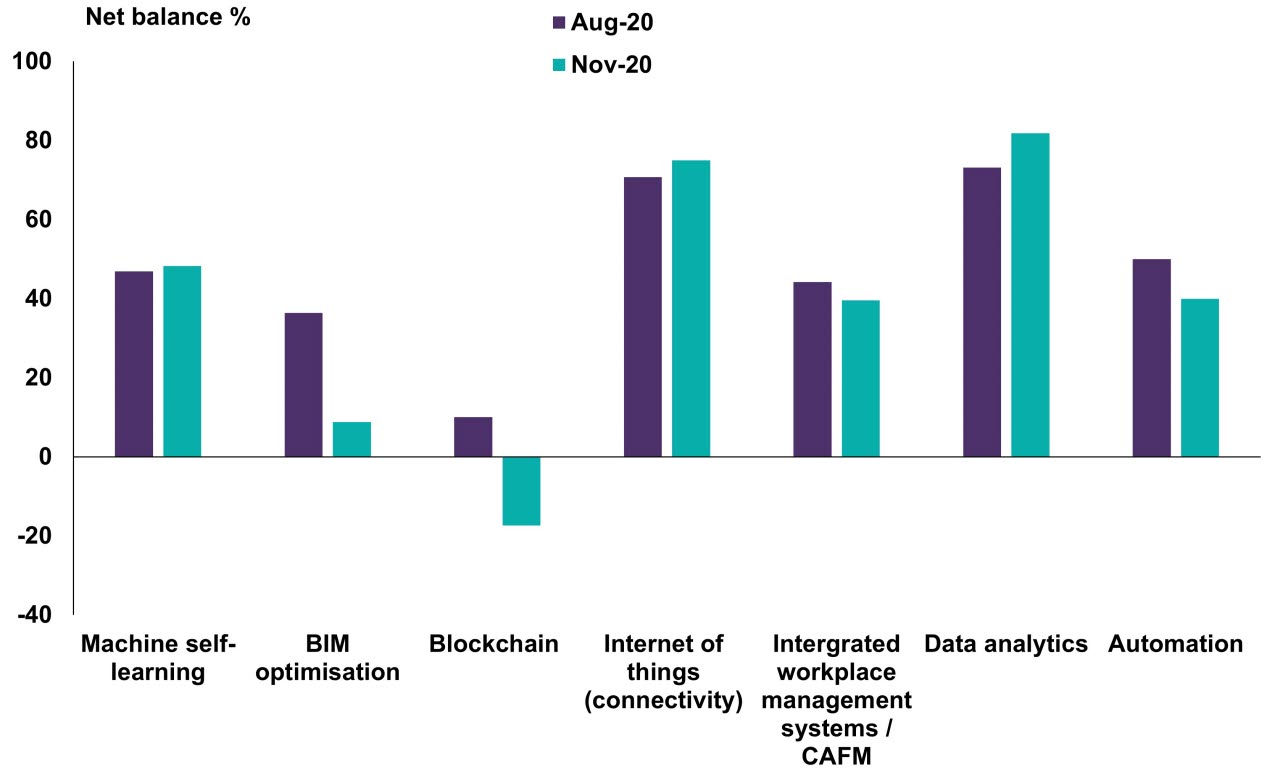

How has investment in technologies changed over the past 12 months?

Respondents noted increased levels of tech investment across the board – with one curious exception. Blockchain is regarded by many experts as having transformative potential for the built environment. Nonetheless, respondents reported only minimal levels of investment in the technology for the first three quarters of the year. In Q4, those modest numbers fell into negative territory (-17% net balance).