Construction output accelerating, but material cost pressures intensify

-

Email

Email

-

Facebook

Facebook

-

Linkedin

Linkedin

-

Twitter

Twitter

-

Whatsapp

Whatsapp

05 August 2021

RICS Global Construction Monitor, Q2 2021

- Construction output accelerating in all global regions, with Europe posting especially strong growth

- Pressures on material costs were highlighted by 83% of respondents as the greatest impediment holding back construction activity

- Positive increases in workloads reported across all sectors, with infrastructure leading the way

- Employment levels set to pick up, with headcounts predicted to rise in the majority of markets, a substantial improvement relative to the same period in 2020

The recovery across the global construction market is gaining pace with the latest feedback to the RICS Global Construction Monitor showing sentiment in all world regions sitting in positive territory once again.

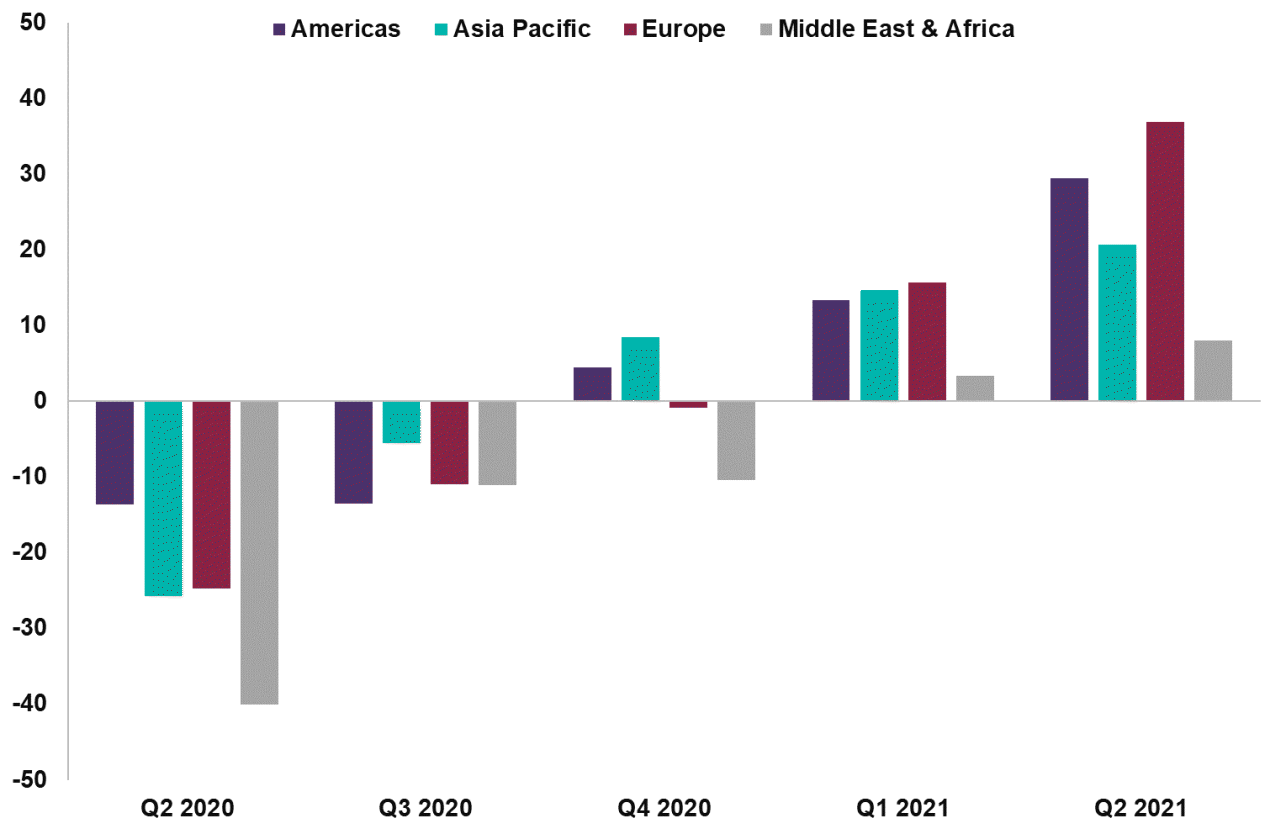

Construction output accelerating in all global regions

At a global level, the RICS Global Construction Activity Index*, a measure of current and expected construction market conditions among construction professionals, has risen to +25 in Q2 2021 up from +14 in Q4 2020. This is a significant increase from the low of -24 in Q2 last year, indicating an acceleration in output growth over the past quarter.

The most notable improvements were seen in Europe (+34) and the Americas (+29), with Asia Pacific (+21) also moving firmly into the expansionary territory and feedback more subdued within the Middle East and Africa (+8).

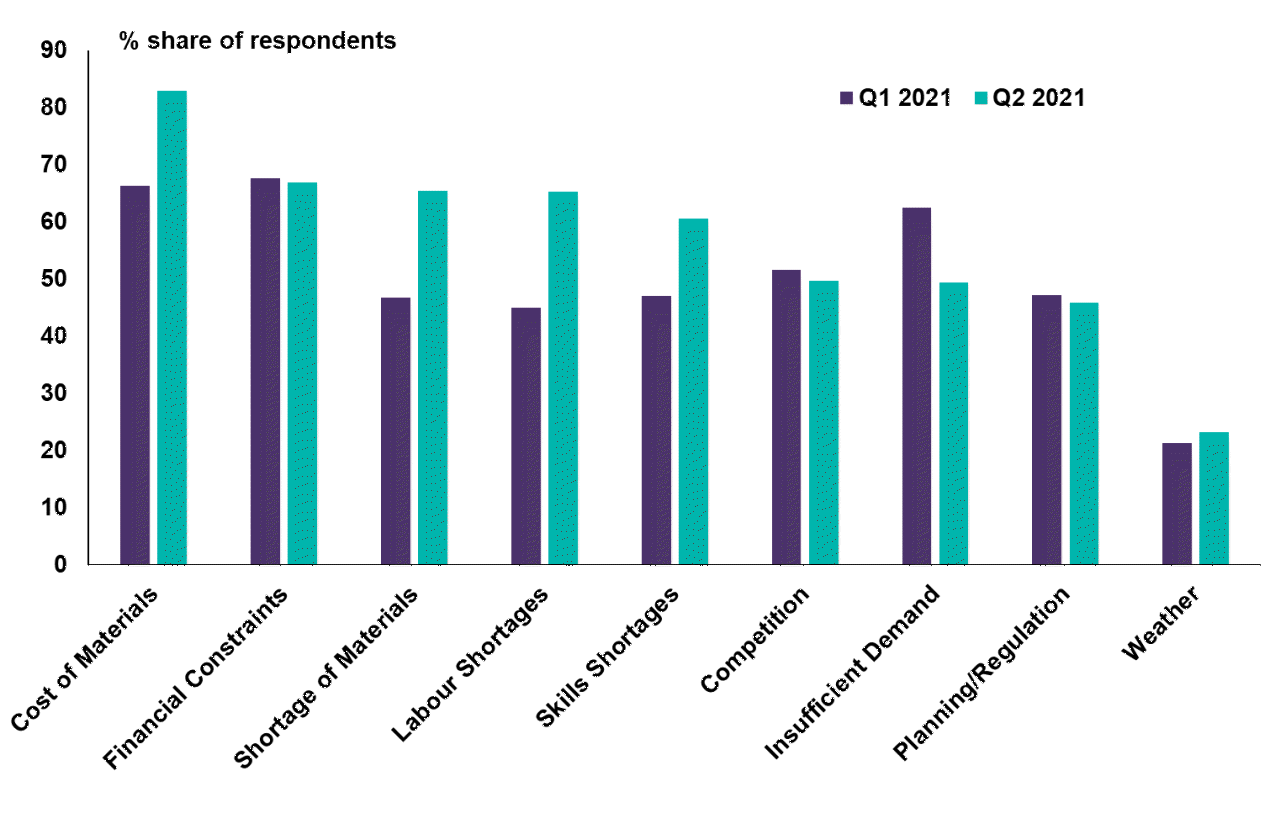

Pressures on material costs highlighted as the greatest impediment holding back construction activity

Despite the overall optimism, rising material costs have been highlighted by 83% of respondents as already holding back construction activity, rising from 66% last quarter. This trend is being seen across the globe, with the pressures intensifying going forward due to bottlenecks in the supply chain and an upsurge in demand continuing to drive costs higher. Along with the concerns on rising material costs, financial constraints, shortages in materials, labour and skills are all noted as impediments to market activity in Q2.

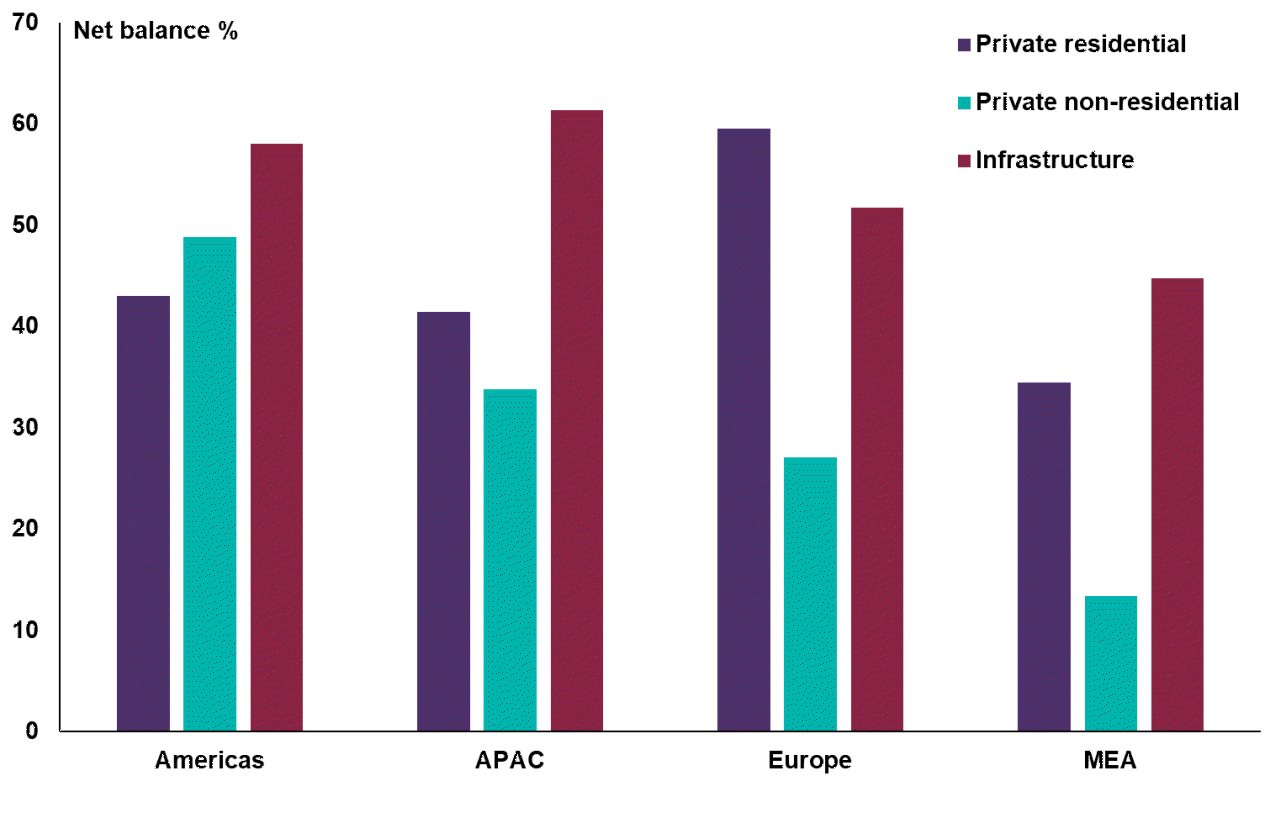

Positive increases in workloads reported across all sectors recorded for first time

Notably in Q2, positive increases in workloads were recorded in all. Growth in infrastructure workloads continue to lead the way, closely followed by private residential with private non-residential, which incorporates all commercial buildings, recording a small pick-up in activity. This represents a significant turning point for the construction market as it continues to emerge from the pandemic. However, with the spread of the Delta variant and the continuing changes as global governments respond, there is note of caution to the speed of recovery.

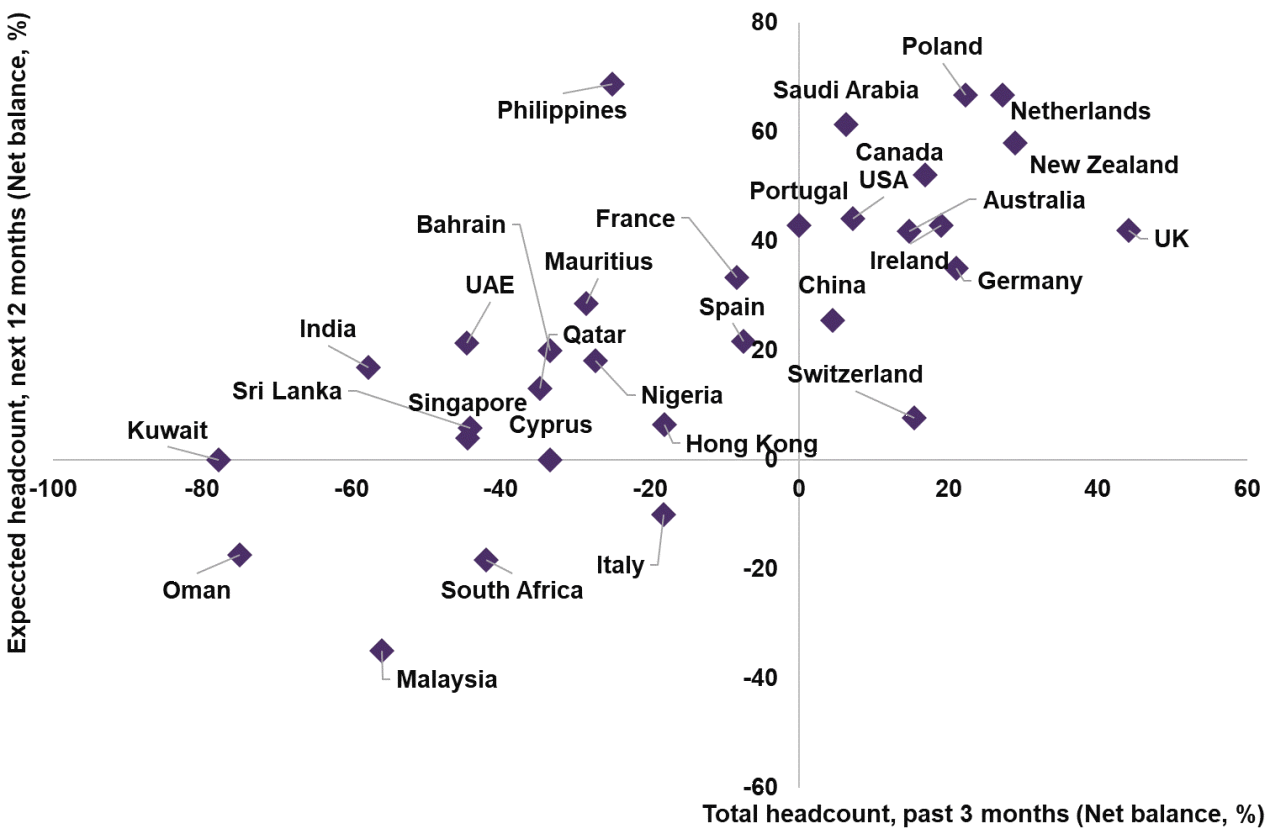

Employment levels set to pick up, with headcounts predicted to rise in the majority of markets

Close to 90% of markets covered by the Monitor have recorded positive expectations for employment over the coming year, a substantial improvement on the same period in 2020, when contributors expected total construction employment figures to fall in most nations. There has been an increase of +27% in respondents predicting headcounts to improve in the next 12 months.

Other key findings from our latest results include:

- At a country level the vast majority of nations covered by the Monitor now exhibit positive readings for the Construction Activity Index* but there are still some markets with more subdued conditions, including Malaysia, Mauritius and Oman. At the other end of the scale, Portugal, the Netherlands, Saudi Arabia and the USA recorded the most elevated readings, citing significant growth in workloads within all sectors.

- Twelve-month workload expectations strengthened across all categories, with infrastructure again leading the way (+57%), followed by private residential (+46%) and private non-residential (+34%) which is expected to grow particularly strongly in the Americas.

- COVID is still seen as an issue across the globe and is noted by many respondents as impacting on the results.

You can read the full report which contains a global overview and in-depth regional analysis here.

Simon Rubinsohn, Chief Economist at RICS, commented:

“Around the globe, the feedback to the RICS Global Construction Monitor from respondents generally shows an improving trend in activity with infrastructure leading the way as government’s look to build a post-COVID economic recovery.

“Aside from COVID, the construction industry is also having to cope with rising material costs reflecting supply chain disruption around key commodities and also from shortages of labour as the sector tries to build capacity. Against this backdrop, construction costs are seen as likely to continue to rise strongly over the next twelve months suggesting that any recovery in profitability in the near term is likely to be hard fought.”

* The Global Construction Activity Index is a weighted composite measure encompassing variables on current and expected market activity as well as margin pressures.